ONC continues to push out more data when it comes to meaningful use, EHR adoption, RECs, and related areas. As a data addict, I could spend forever looking through and analyzing this data. So, I’ll probably do a series of posts across Healthcare Scene over the next couple weeks looking at the charts and data that ONC has made public about meaningful use and EHR adoption. I know some of the charts have been out for a while, but the analysis should still prove useful.

If you want to join in on the analysis of this data, I welcome you in the comments of each post. Plus, if you want to find your own nuggets to share, I’d suggest starting with their quick stats and dashboards pages.

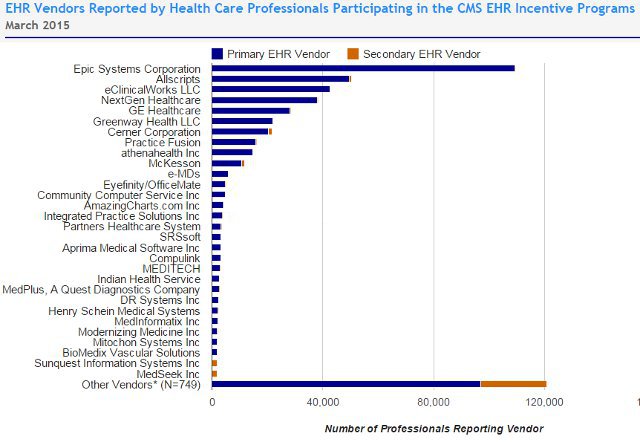

First up in our look at the ONC EHR data is a look at the meaningful use participation chart for ambulatory EHR vendors (eligible providers if you prefer):

The most important part of this chart to me is that the two largest bars on the chart. The largest bar is the 749 “Other EHR Vendors” category at the bottom of the chart. It’s easy to miss this bar, but I believe it’s extremely important to note how big the long tail is when it comes to ambulatory EHR adoption. I’ve often said that it doesn’t take that many doctors to make yourself a decent EHR business. This chart illustrates how many EHR vendors are still in the game. There are only 3 EHR vendors that have over 40,000 providers. I know that many think that EHR vendor consolidation is bound to happen. Some certainly will, but I don’t see it happening at a massive scale in the ambulatory EHR world.

The second largest bar on the chart is the Epic EHR adoption. What’s important about this bar is that this totally represents that hospital owned ambulatory EHR adoption. Epic does not and will not sell Epic directly to a small ambulatory provider. All of these “eligible providers” for Epic are in hospital systems. I take away two important things from this. First, we see in plain sight how big the roll up of ambulatory practices is by hospitals. Second, this chart illustrates the opportunity that Cerner and Meditech have available to them. As you’ll see in the next chart, Cerner and Meditech have more hospital installs than Epic, but they’re much farther down on the ambulatory side. A look at history explains why they’ve had trouble penetrating the ambulatory market, but I believe it’s a huge opportunity for them going forward.

I’ll be interested to see how this chart continues to evolve over time. Will we doctors leaving hospitals to go back on their own shift the balance of power? Will we see massive EHR consolidation? I also can’t help but note Read more from originating source…